Many startups and growing companies are dreaming about an IPO or getting the big investor on board to grow the company to unicorn status and beyond. Companies are often ready with an amazing product and great business KPIs, but the major challenge is to have full, compliant, and representative financial statements to provide transparent and trusted insight into the company's financials.

Producing a set of US GAAP/IFRS compliant financial statements is not mandatory and not a major focus point in the earlier stages of growth, but the later you start getting ready for it, the more difficult and costly it becomes. At Mews, we started early to make sure we have no surprises later. Here are some best practices on how to make sure you are ready for the big investors.

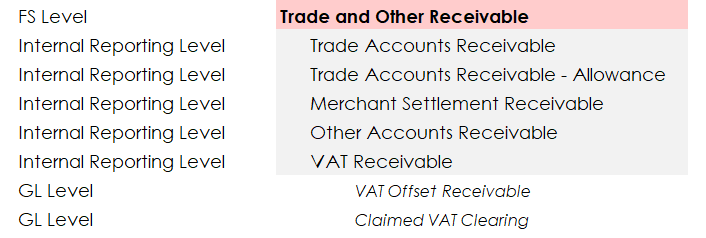

Set up your chart of accounts

The first step is always defining your reporting structure. The US GAAP/IFRS financial statements are usually reported on a very low level of detail, with more details being reported further in the disclosures. Design your chart of accounts in levels that are rolling up into each other, where the top level details the actual financial statements, the lower one is on the level of required disclosures, and the lowest one is on the level of analytics you need to review your financials on a day-to-day basis.

Example of financial reporting account structure

Create mapping logic

Once you have your chart of accounts you can look into your General Ledger. Based on the structure in which your accountants maintain their records (which will be informed by the nature of your accounts), start mapping these into your chart of accounts.

During this exercise you often find that your accounting is not maintained in a way that provides the required structure of information. Don’t panic. Work with your accountants on how to change the accounting processes to fit into the company’s chart of accounts.

Once you have the mapping ready, save it in a standardized bridge so you can use it for any new accounts or entities which will flow smoothly into your accounting.

Reconcile your balance sheets

In their very early stages, companies look at the balance of their bank account to understand how they are performing. Later on, the profit and loss reports are the key ones needed to run the business. But often the balance sheets are left behind as a not-so-important piece of reporting (“I know my bank account balance, so what else do I care?”), but the opposite is true.

The balance sheet is a source of important business information, like working capital, leverage, debt/equity ratio, liquidity, and many others. But it is a key control point for the accuracy of your profit and loss report as well. Historical accruals that were forgotten to be released make your profit worse than it is, or items pending on a suspense account may be missing in your revenues.

Finally, your balance sheets are the key to your future financial statements.

In order the keep the balance sheet under control, make sure that there’s a regular reconciliation process in place, where every single GL account is reconciled on a regular basis and your accountants can explain every single balance with external supporting documentation. If you don’t start early, reconciling and cleaning up the accounts can take months or even years depending on how complex your business is.

Set up consolidation process and tools

If your business is not run by one single entity, but by multiple entities, the consolidation process may be a major challenge for the finance team. To be able to consolidate properly, you should set up a process of regular intercompany reconciliation and make sure you have your equity reconciled up to every single dollar. These are the key items to set up a proper intercompany elimination process.

The actual elimination and consolidation can be done in excel spreadsheets in the early stages, but the right consolidation software or customized ERP is a great investment, especially for companies with larger structures.

Hire the right team

Once you have your accounting data clean and your balance sheets and profit and loss reports are finetuned, you can finally start preparing the actual financial statements. Writing down your policies, explaining balances, and making sure all information is presented in the financial statement in a way that is compliant with required accounting standards.

This is an extremely complex and time-consuming process, and you need to make sure you have the right people to do it. External advisors are usually very expensive, they never have full internal business knowledge, and the fluctuation in the team does not ensure continuity.

At Mews, we started with hiring experienced individuals at a very early stage and now we have a team fully dedicated to the work related to audits and financial statements. It was a great investment that’s now really paying off.

Example of finance team structure with separate Consolidation team

Cooperate with your auditors

The ultimate authority that will assure your investors that the financial statements are correct and compliant are the auditors. Financial teams are often scared and try to hide things from auditors, but they are here not to punish you for your mistakes. They’re here to help you to make sure your financials are accurate.

If you find the right audit team, be open and transparent, and don’t be afraid to discuss and ask about things where you are not confident. You have the same goal as the auditors do – produce accurate and compliant financial statements.

Involve your marketing team

Once you have everything prepared and all the hard work done, it’s time to make sure that you impress your investors on the first look. The numbers and accounting are not often exciting, but if it is presented in nice corporate colors, cool design, and it’s easy to read, that's a completely different story. Moreover, the financial statements are the trademark of every finance team, so make sure you present yourself well. So take time with your marketing team and make sure you finetune the presentation to the top level.

Written by

Martin Olsovsky

Martin joined Mews in 2018 after a decade of experience in finance and consulting. Now, he keeps all of us and our financials in line as Mews' Finance Director.